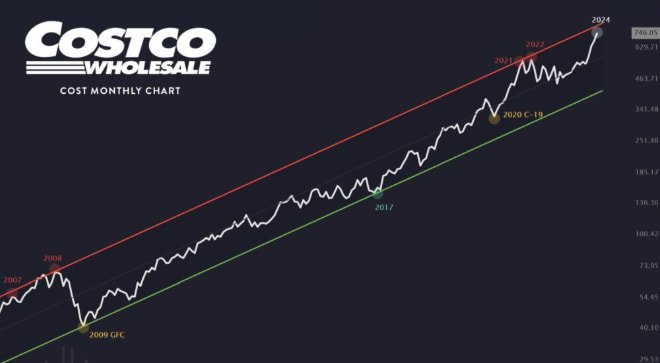

Editor’s Note: Costco (COST) serves as a premier defensive stock offering long-term stability through its recurring membership revenue model, resilient consumer demand and a relentless focus on operational efficiency that sustains growth even during economic downturns.

The core thesis for Costco (COST) as a long-term holding rests on its unique Blue Ocean positioning: it doesn’t just sell goods; it sells a membership-based lifestyle that insulates the company from the volatility of traditional retail cycles.

By maintaining razor-thin margins on high-quality products and generating massive cash flow from loyal members, Costco creates a self-reinforcing financial flywheel that is exceptionally difficult for competitors like Walmart or Amazon to replicate.

Investors’ Experience

Many investors feel a palpable sense of anxiety when market indicators signal a potential recession, often asking themselves, “Is my portfolio truly diversified, or am I overexposed to economic sensitivity?” It is completely natural to feel this hesitation; watching macro-economic shifts can make one feel like they are bracing for a storm without a sturdy roof.

However, looking at Costco is not just about analyzing a ticker symbol; it is about observing a company that has turned the necessity of “value” into a permanent competitive advantage. When you analyze Costco, you aren’t just looking at a retailer; you are looking at a system of human trust and logistical brilliance that remains robust when the rest of the market creates panic.

The Costco Business Model

Costco’s membership-based model is the company’s primary economic moat, transforming the traditional retail relationship into a recurring, high-margin subscription service that prioritizes customer loyalty over short-term transactional profit.

Unlike traditional retailers that rely solely on product markup, Costco derives a significant portion of its operating income from annual membership fees. This structure allows the company to cap product markups at approximately 14-15%, ensuring that the prices offered to members remain consistently lower than those of competitors.

This pricing discipline creates a virtuous cycle: lower prices attract more members, more members increase the volume of goods sold, and that volume, in turn, allows Costco to negotiate even better pricing from its suppliers. It is a system that effectively turns the “race to the bottom” in retail into a “race to the top” in terms of member value and retention.

Renewal Rates and Consumer Discretionary

This membership-driven approach is further reinforced by the high renewal rates, which typically hover around 90-92% in the U.S. and Canada. This predictability is a luxury rarely seen in the consumer discretionary sector, where customer acquisition costs are notoriously high.

By focusing on retaining existing members rather than constantly chasing new, expensive leads, Costco optimizes its marketing spend and funnels those savings back into the business. For investors, this creates a reliable, recession-resistant revenue stream that acts as a stabilizer, even when broader retail sectors experience contractionary pressure.

Recurring Revenue and Customer Loyalty

The stability of Costco’s recurring revenue provides a predictable “floor” for its earnings, decoupling its financial performance from the erratic spikes and drops associated with seasonal retail trends.

This predictability is powered by the Kirkland Signature brand, which has successfully bridged the gap between premium quality and warehouse pricing. Because members trust that private-label products will rival national brands in quality, they are more likely to consolidate their shopping at Costco, increasing their “wallet share” within the store.

This loyalty is not just sentimental; it is a calculated economic decision by the consumer, which strengthens Costco’s position as a primary household budget manager.

Inventory Efficiency and Margin Strategy

By intentionally limiting its product assortment to approximately 4,000 carefully curated items, Costco achieves an inventory turnover rate that is significantly faster than that of its peers, which optimizes cash flow and mitigates the risk of unsold stock.

In a world of infinite choice, Costco’s “less is more” strategy is a masterclass in efficiency. Because they carry fewer SKUs, they have higher purchasing power for the items they do carry, enabling them to command deeper discounts from manufacturers.

This operational efficiency is passed on to the consumer, further reinforcing the value proposition that makes Costco an essential stop for households looking to manage their budgets effectively in inflationary or recessionary environments.

Financial Health and Recession

Costco’s status as a defensive asset is supported by a robust balance sheet and the empirical observation that its comparable sales tend to remain stable—or even accelerate—as consumers become more value-conscious during economic downturns.

When economic conditions tighten, consumer behavior shifts toward value. Research has consistently shown that Costco benefits from this “K-shaped” economic dynamic, where even households in higher income brackets look for ways to optimize their spending.

Because Costco’s average member is often more affluent than the average shopper at other big-box retailers, the company maintains a level of spending resilience that allows it to outperform during periods of volatility. This demographic advantage provides a buffer against the typical cyclicality that plagues other retail stocks.

Navigating Economic Cycles

The company’s recession-resilient nature is amplified by its gasoline business, which acts as a “traffic driver” and keeps members engaged with the warehouse, even when they aren’t planning a major grocery run.

Gasoline sales represent roughly 10% of total revenue, but their strategic importance is far greater than the margin they produce. The lower price point at the pump is a visible sign of Costco’s value, which creates an immediate “hook” to get members onto the property.

Once they are there for gas, the probability of them entering the warehouse to perform a “cross-shop” increases dramatically. This creates a powerful flywheel effect that keeps warehouse foot traffic consistently high, regardless of the broader economic environment.

Balance Sheet Strength and Capital Allocation

Its history of managing excess cash through strategic special dividends demonstrates a shareholder-friendly approach that focuses on returning value without compromising the core business’s growth trajectory.

As of recent fiscal quarters, it has maintained a significant cash pile, providing a cushion for both operational stability and future distributions. Unlike companies that over-leverage to pursue growth, Costco’s approach to capital is measured and conservative.

This conservative posture has historically served investors well, as it ensures the company can weather any unforeseen macro-economic “black swan” events while maintaining its dividend growth.

Below is a summary of why Costco’s financial structure stands out:

| Metric | Advantage |

| Membership Revenue | Provides high-margin, recurring income floor. |

| Inventory Turnover | High speed minimizes capital tied in stock. |

| Balance Sheet | Low debt-to-equity keeps risk profiles low. |

| Dividend History | Regular growth plus potential for special payouts. |

Future Growth and Competitive Moat

Its long-term growth is anchored by its global expansion strategy and its successful transition into the digital arena, which serves as a new growth vector for younger, tech-savvy demographics.

While warehouse expansion remains the engine of the business, the digital evolution—specifically the digital flywheel—is becoming a critical differentiator. By integrating digital features like inventory tracking and online delivery services, it is removing the friction that once kept some shoppers away. This transformation is not about replacing the warehouse experience; it is about extending it.

By capturing the digital-first shopper, Costco is future-proofing its membership base, ensuring that it remains relevant to the next generation of consumers.

The competitive moat is further widened by the sheer scale of Costco’s operations. Establishing a supply chain as efficient as Costco’s requires decades of investment and logistical perfection. It is a classic “barrier to entry” scenario: even if a competitor has the capital, they lack the relationships and the proprietary systems that Costco has refined over 40+ years.

This deep-rooted advantage makes Costco a “moat-heavy” business that is exceptionally well-positioned to maintain its leadership in the retail sector for the coming decades.

Global Expansion and Digital Transformation

International expansion presents a massive, untapped opportunity, as the “Costco model” has demonstrated universal appeal, regardless of geographical or cultural market nuances.

Markets in Europe, Asia, and Latin America are increasingly showing an appetite for the Costco value proposition. As the company continues to refine its localization strategies—adapting products to regional preferences while maintaining the core warehouse identity—it unlocks new growth markets. This international diversification is a hedge against localized economic downturns, further smoothing the company’s long-term performance profile.

Assessing Valuation and Investment Risks

While Costco often trades at a premium P/E ratio compared to other retailers, this “quality premium” is justified by the company’s consistent earnings growth and its superior risk-adjusted returns over time.

Investors often debate whether Costco is “overpriced” given its high multiple. However, viewing Costco through the lens of a “growth stock” misses the point. It is a “quality compounder.” When you pay a premium for Costco, you are paying for the certainty of its cash flows and the safety of its business model.

While risks such as tariff-related cost pressures or labor wage increases exist, Costco’s ability to manage margins has historically allowed it to pass through or absorb these costs more effectively than its peers.

FAQ on Costco (COST) Stock

Is Costco (COST) considered a recession-proof stock?

Yes, Costco is widely regarded as a defensive asset. Its membership-based model and focus on value-driven bulk products make it an attractive destination for consumers during economic downturns, helping to sustain revenue even when overall retail spending slows.

What is the primary driver of Costco’s long-term growth?

The primary drivers are membership fee income and consistent comparable sales growth. The high renewal rates, combined with the company’s ability to expand both warehouses globally and digital capabilities, create a sustainable compounding effect on earnings.

Why do analysts consider Costco an expensive stock?

Costco typically trades at a high P/E ratio compared to other discount retailers. This is often described as a “quality premium,” where investors are willing to pay more for a business with a proven, highly predictable, and recession-resilient financial profile.

How does the gasoline business impact Costco’s stock?

Gasoline acts as an engagement “flywheel.” By offering low-cost fuel, Costco drives consistent traffic to its warehouses. This increased foot traffic results in higher cross-shopping rates for groceries and household items, boosting overall customer lifetime value.

Should I worry about competition from Amazon or Walmart?

While competition is always a factor, Costco’s unique warehouse-club model is distinct. Its focus on a limited, curated product assortment and private-label Kirkland Signature dominance creates a different value proposition that has historically coexisted successfully alongside big-box competitors.

Disclaimer: This analysis is for informational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.